Life insurance after a heart attack can feel difficult, but a past cardiac event does not automatically end your chances of approval. Insurers want to understand what happened, how well you recovered, and whether your current health appears stable. A strong application presents those facts clearly instead of leaving underwriters to guess.

The outcome can range from standard coverage to a higher premium, a temporary postponement, or a limited benefit policy. Every insurer uses its own guidelines, so one decision does not represent the entire market. This guide explains the process, likely costs, policy choices, and practical steps that may improve your result.

Can You Get Life Insurance After a Heart Attack?

Yes, many people obtain life insurance after a heart attack. Approval depends on the severity of the event, treatment, recovery, age, and other health conditions. Insurers also look at the time since the heart attack because recent events may not provide enough evidence of long term stability.

An underwriter may approve coverage with a higher risk class, postpone the application until more follow up is available, or decline it. Simplified issue and guaranteed issue policies may remain available when traditional underwriting is difficult, although they often cost more for less coverage.

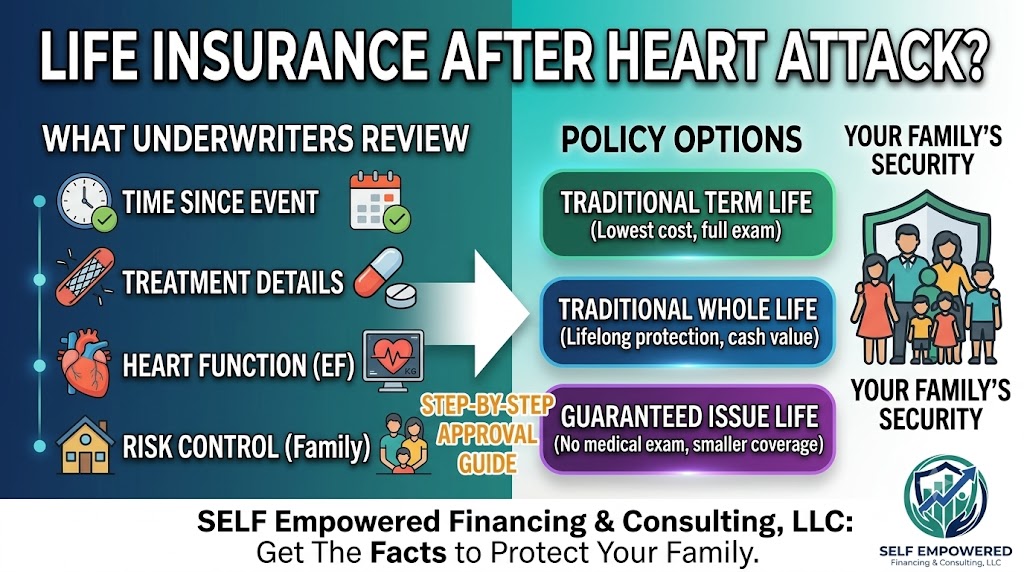

What Life Insurance Underwriters Review

Underwriting is the process insurers use to decide eligibility and pricing. Traditional underwriting may include an application, medical records, prescription history, blood and urine testing, and a physical exam. Accelerated underwriting may remove the exam but still use outside data and health information.

For life insurance after a heart attack, the underwriter usually wants a complete picture rather than one diagnosis. A clear cardiology history can help the insurer separate an old, stable event from an ongoing risk.

Key Cardiac Underwriting Factors

| Factor | What the Insurer May Review | Why It Matters |

|---|---|---|

| Time since the event | Date of the heart attack and recovery period. | More follow up can show whether health is stable. |

| Treatment | Medication, stent, angioplasty, bypass surgery, or other care. | Treatment details help explain the cause and current condition. |

| Heart function | Cardiology notes, imaging, stress testing, and ejection fraction. | Results can show remaining damage and exercise capacity. |

| Risk control | Blood pressure, cholesterol, blood sugar, weight, and tobacco use. | Controlled risk factors may support a better assessment. |

| Follow up | Cardiology visits, cardiac rehabilitation, and medication adherence. | Consistent care shows active management of heart health. |

Age, diabetes, repeated cardiac events, kidney disease, and tobacco use may also affect the decision.

When Should You Apply?

There is no universal waiting period for life insurance after a heart attack. Some companies may postpone a recent case until recovery, testing, and follow up are documented. Applying too soon can produce a decision based on incomplete information, while waiting can provide stronger medical evidence.

Medical Records and Tests That May Matter

Accurate records can make life insurance after a heart attack easier to evaluate. Underwriters may request an attending physician statement from your cardiologist or primary doctor. Missing records can delay the process because the insurer cannot confirm the event, treatment, or recovery.

Useful information may include:

- The hospital discharge summary and date of the heart attack.

- Details of angioplasty, stents, bypass surgery, or medication treatment.

- Recent cardiology notes and a current medication list.

- Results from an electrocardiogram, echocardiogram, stress test, or other cardiac testing.

- Blood pressure, cholesterol, blood sugar, kidney function, and weight trends.

- Proof of cardiac rehabilitation when recommended.

- Clear documentation of tobacco use or successful cessation.

Policy Options After a Cardiac Event

The right policy depends on coverage needs, budget, and underwriting availability. Traditional term insurance may provide the most death benefit per premium when approved. Permanent coverage may support lifelong needs, final expenses, or legacy planning.

Comparing Common Life Insurance Options

| Policy Type | Typical Underwriting | Main Tradeoff |

|---|---|---|

| Traditional term life | Full or accelerated review with detailed health questions. | Lower starting cost may be available, but cardiac history can increase premiums. |

| Traditional whole life | Medical review with permanent coverage and cash value. | Premiums are usually higher, but coverage can last for life under policy terms. |

| Simplified issue life | Health questions with limited or no exam. | Approval can be easier, but coverage may cost more. |

| Guaranteed issue life | No health questions for eligible ages. | Coverage is usually smaller and may include a graded death benefit period. |

| Employer group life | Limited individual underwriting within plan rules. | Coverage may be tied to employment and may not meet the full need. |

Important: No medical exam does not always mean no medical review. Some accelerated or simplified applications may use prescription records, claims data, or other sources. Read the application carefully and answer every question truthfully.

How a Heart Attack Can Affect True Costs

The cost of life insurance after a heart attack depends on age, coverage amount, policy type, tobacco status, recovery, and overall health. A company may offer a standard rate, a table rated premium, or an extra charge. Another company may postpone or decline the same applicant.

Table ratings increase the base premium to reflect higher risk. The exact increase varies by insurer and rating. Simplified issue and guaranteed issue plans can also carry a higher cost for each dollar of death benefit because the insurer has less medical information or accepts broader risks.

Steps That May Strengthen an Application

You cannot erase a past event, but you can present current health accurately. The following actions may help an underwriter understand your progress:

- Follow the treatment plan created by your health care team.

- Attend recommended cardiology visits and cardiac rehabilitation.

- Take medications as prescribed and keep records current.

- Work with your doctor to manage blood pressure, cholesterol, and blood sugar.

- Avoid tobacco and disclose past use honestly.

- Prepare a short timeline of the event, treatment, recovery, and current activity.

- Apply through someone who can compare multiple underwriting guidelines.

Common Application Mistakes to Avoid

A rushed application can make life insurance after a heart attack harder than necessary. Do not minimize the event, guess at dates, or leave out medication. Insurers may verify health information, and inconsistent answers can cause delays or concerns about accuracy.

Do not cancel existing coverage until new coverage is approved, delivered, reviewed, and active. A new application can still change before final issue if health changes or requirements remain incomplete.

Could Whole Life Insurance Be a Practical Option?

Whole life insurance may suit people who want permanent protection, predictable scheduled premiums, and contractual cash value. It can be considered for final expenses, legacy goals, or lifelong obligations. Approval and price still depend on the insurer and the applicant.

Self Empowered Financing & Consulting, LLC. can help you explore whole life insurance solutions and compare them with term or limited underwriting options. The goal is not to force a permanent policy. It is to match coverage with your needs, health history, and budget.

How Self Empowered Financing & Consulting, LLC. Can Help

Shopping for life insurance after a heart attack can become frustrating when different insurers give different answers. Self Empowered Financing & Consulting, LLC. helps organize the case, identify realistic options, and explain tradeoffs in plain language.

A consultation for life insurance after a heart attack reviews the event date, treatment, medications, follow up, coverage goal, budget, and existing insurance. This information helps narrow the market before a formal application.

Before applying, gather policy statements, beneficiary details, and information about any current workplace coverage. Decide how much protection your family would need for income replacement, debts, final expenses, education, or business obligations. Clear goals help prevent overbuying and make it easier to compare term length, permanent coverage, premium guarantees, conversion options, riders, and long term affordability.

Frequently Asked Questions

Will Every Insurer Decline Me After a Heart Attack?

No. Insurers use different underwriting guidelines. One may postpone or decline an application while another may offer coverage at a higher premium. The result depends on the complete medical history and current stability.

Can I Get Coverage Without a Medical Exam?

Possibly. Accelerated, simplified issue, and guaranteed issue products may not require a traditional exam. They can still use health questions or outside data, and easier underwriting may mean higher costs or lower coverage.

Does Cardiac Rehabilitation Help My Application?

Cardiac rehabilitation is a medically supervised recovery program. Completing recommended care can provide evidence of follow through, but it does not guarantee approval. Underwriters consider the entire case, including test results and risk factor control.

Conclusion

Getting life insurance after a heart attack is possible for many people, but the process requires realistic expectations. The insurer will look beyond the diagnosis to treatment, heart function, risk control, recovery, and ongoing care.

Prepare accurate records, compare underwriting approaches, and choose a policy that fits the real financial need. Do not hide medical information or replace existing coverage too early.

Self Empowered Financing & Consulting, LLC. can help you review available options and plan the next step. Schedule a personalized life insurance consultation to discuss your goals, heart history, and budget with greater clarity.