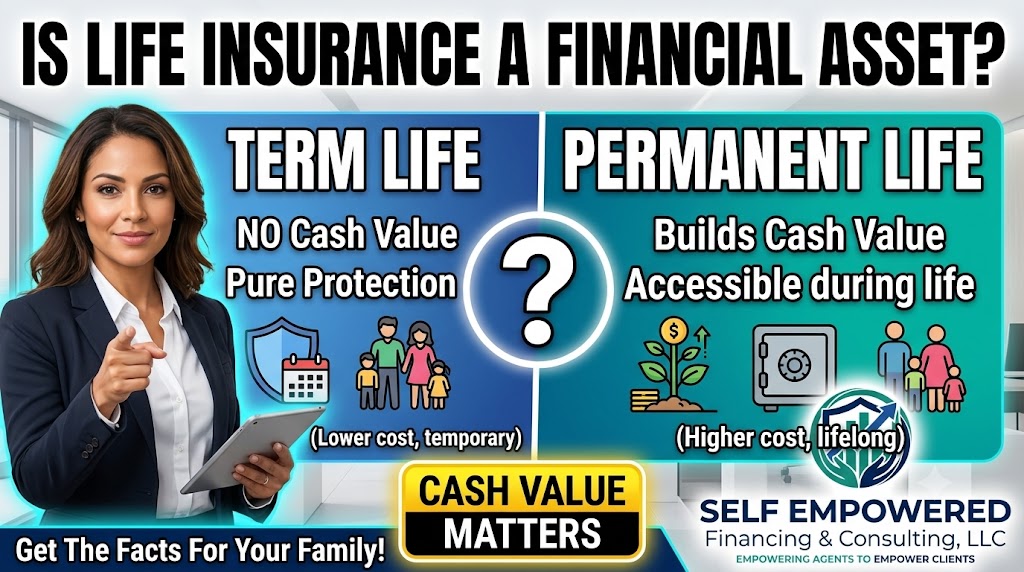

Is life insurance considered an asset when you review your personal finances? The answer depends on the policy. Term life insurance normally provides protection only and does not build accessible value. Permanent life insurance may build cash value, which can become part of your broader financial picture.

An asset clearly provides measurable economic value. Savings, investments, property, and business interests may appear on a net worth statement. Certain life insurance policies can also appear there when they have a current value that can reasonably be measured.

Self Empowered Financing & Consulting, LLC. helps families look beyond the policy label.

What Makes Something a Financial Asset?

A financial asset is something you own that has economic value. It may grow, be sold, or provide access to money. Liquidity matters too. Cash is highly liquid, while property may require time or borrowing to unlock its value.

So, is life insurance considered an asset under this definition? It can be, but the policy must provide more than a future death benefit. A policy with cash value gives the owner a measurable interest during life. That value may be available through a withdrawal, policy loan, surrender, or life settlement.

The death benefit is generally a future benefit for beneficiaries. For personal net worth calculations, cash surrender value is usually more relevant than the full death benefit.

Term Life Insurance Versus Permanent Life Insurance

The easiest way to answer whether life insurance is considered an asset is to compare term and permanent coverage.

| Feature | Term Life Insurance | Permanent Life Insurance |

|---|---|---|

| Coverage period | A set number of years. | Potentially a lifetime. |

| Cash value | Usually none. | May build over time. |

| Typical premium | Lower at first. | Usually higher. |

| Net worth treatment | Usually not listed. | Cash surrender value may be listed. |

| Main purpose | Temporary protection. | Protection plus cash value. |

| Access during life | Usually limited. | Loans, withdrawals, or surrender may be available. |

Term insurance can still be essential. It may protect a family during working years, cover a mortgage, or support children. Because it normally has no cash value, it is generally treated as a protection expense rather than an owned asset.

Permanent coverage includes whole life, universal life, indexed universal life, and variable life. These products differ in guarantees, costs, and risk. Their cash value can make them an asset, although value may be modest during early years.

Why Cash Value Changes the Answer

When people ask whether life insurance is considered an asset, they are often asking about cash value. Cash value accumulates inside certain permanent policies after policy costs and charges. Its growth depends on the contract.

Whole life insurance commonly offers scheduled premiums, guaranteed cash value growth, and a guaranteed death benefit when requirements are met. Some participating policies may pay nonguaranteed dividends. Universal life offers flexibility, while variable life uses investment choices that can rise or fall.

You can learn more about whole life insurance options and how lifelong protection may fit into a broader plan.

Cash value can support several planning needs:

- Funds for an unexpected expense.

- Supplemental retirement liquidity.

- Business or succession planning.

- Education or family support.

- Legacy planning for beneficiaries.

- A reserve with contract based features.

Important: A policy loan is not free money. Interest is charged, and unpaid loans can reduce the death benefit. Large loans can increase lapse risk. Withdrawals may reduce value and coverage. Tax consequences may arise after surrender, lapse with a loan, or modified endowment contract treatment.

How Life Insurance May Appear on a Net Worth Statement

Is life insurance considered an asset for a personal balance sheet? A permanent policy may be listed at its current cash surrender value. This is the amount the owner would receive after applicable charges and adjustments if the policy ended today.

Do not list the full death benefit as a current asset in a standard net worth calculation. It is generally paid after death and may be reduced by loans. It has an important protection role, but it is not normally current spending money for the owner.

A lender, accountant, or financial professional may use different reporting rules. Ask which value is required and request a current policy statement from the insurer.

Life Insurance Compared With Common Assets

The following comparison shows why a cash value policy can be useful while behaving differently from traditional assets.

| Asset | Liquidity | Growth Potential | Main Risk | Planning Role |

|---|---|---|---|---|

| Savings account | High | Low | Inflation | Emergency cash |

| Investment portfolio | Medium to high | Moderate to high | Market losses | Growth and retirement |

| Real estate | Low | Varies | Market and selling costs | Equity and income |

| Permanent life insurance | Medium, subject to policy terms | Contract dependent | Costs and lapse risk | Protection, cash value, and legacy |

| Term life insurance | No cash value | None | Coverage may expire | Temporary protection |

This comparison explains why life insurance cannot receive the same asset treatment for every household. A permanent policy may provide stability and tax advantages, but it is not a replacement for emergency savings, diversified investments, or retirement accounts.

Potential Benefits in Financial Planning

A properly designed permanent policy may support a financial strategy. The death benefit can help beneficiaries replace income, pay debts, cover final expenses, or preserve other family assets.

Cash value adds another layer. Depending on the policy, growth may be tax deferred under current federal rules. Owners may access value through loans or withdrawals. Death benefits paid because of the insured person's death are generally excluded from federal gross income, although interest and special situations may be taxable.

Certain whole life policies offer contractual guarantees. This may suit people seeking stability beside market based assets. Insurance does not need to outperform every investment. Its value may come from combining protection, cash accumulation, and legacy planning.

Risks and Limitations to Review

Before deciding whether life insurance is considered an asset in your plan, review the tradeoffs carefully.

- Permanent insurance usually costs more than term insurance.

- Cash value may grow slowly during early years.

- Surrender charges can reduce available value.

- Loans and withdrawals can lower the death benefit.

- An underfunded policy may lapse.

- Variable policies expose value to investment risk.

- Illustrations include guaranteed and nonguaranteed values.

- Tax treatment depends on policy activity and circumstances.

Affordability deserves attention. A policy supports a plan only when you can maintain it. Buying more coverage than your budget can handle may cause cancellation before benefits develop. Review guarantees, illustrated values, fees, loan rates, and surrender periods.

When Life Insurance May Fit Your Strategy

Is life insurance considered an asset worth adding to your plan? It may fit when you need permanent coverage and can comfortably fund the policy after covering basic priorities. These often include emergency savings, debt management, health coverage, and retirement saving.

Permanent life insurance may be worth discussing when:

- You have a lifelong dependent.

- You want to leave a predictable legacy.

- You need liquidity for estate or business planning.

- You have built a strong savings foundation.

- You value guarantees and understand the costs.

- You want coverage without a fixed ending date.

Term insurance may be more efficient when your need is temporary, your budget is limited, or your goal is maximum death benefit for a lower initial premium. Many families use both types.

Questions to Ask Before Buying

A good decision starts with clear questions. Ask for guaranteed and current projections. Confirm how long premiums are required, what happens if you pay less, and how loans affect the policy. Review cash surrender value for each year.

Also ask:

- Which values are guaranteed?

- What fees or surrender charges apply?

- How is interest or a dividend determined?

- What happens if I stop paying premiums?

- Could a loan cause the policy to lapse?

- How will this coordinate with my other assets?

- What assumptions are used in the illustration?

Review the policy every year. Family, business, retirement, debt, and health changes can affect its role. Update beneficiaries and compare performance with the original goals.

Final Answer: Is Life Insurance Considered an Asset?

Is life insurance considered an asset? Term life insurance is generally not an asset because it normally has no cash value. Permanent life insurance can be an asset when it builds cash value that belongs to the owner. For net worth purposes, cash surrender value is usually the most practical figure.

The better question is whether the policy improves your complete financial plan. Cash value alone does not make a policy suitable. Coverage must match your needs, premiums must remain affordable, and the policy should work beside savings, investments, retirement accounts, and estate plans. Therefore, whether life insurance is considered an asset should be answered in the context of your goals.

Get a Personalized Insurance Review

Self Empowered Financing & Consulting, LLC. can help you review protection goals and understand how permanent coverage may support financial security.

Contact the team for a personalized insurance review and discuss a strategy designed around your family, budget, and long term priorities.